Cash Out Refinance Near Me: Rates, Requirements, Steps

You've built equity in your home. Now you want to use it, maybe to consolidate debt, fund a renovation, or invest in another property. So you search cash out refinance near me, expecting straightforward answers. Instead, you get a wall of ads, generic rate tables, and lender pages that all sound the same. None of them tell you what actually matters: whether this move makes financial sense for your situation.

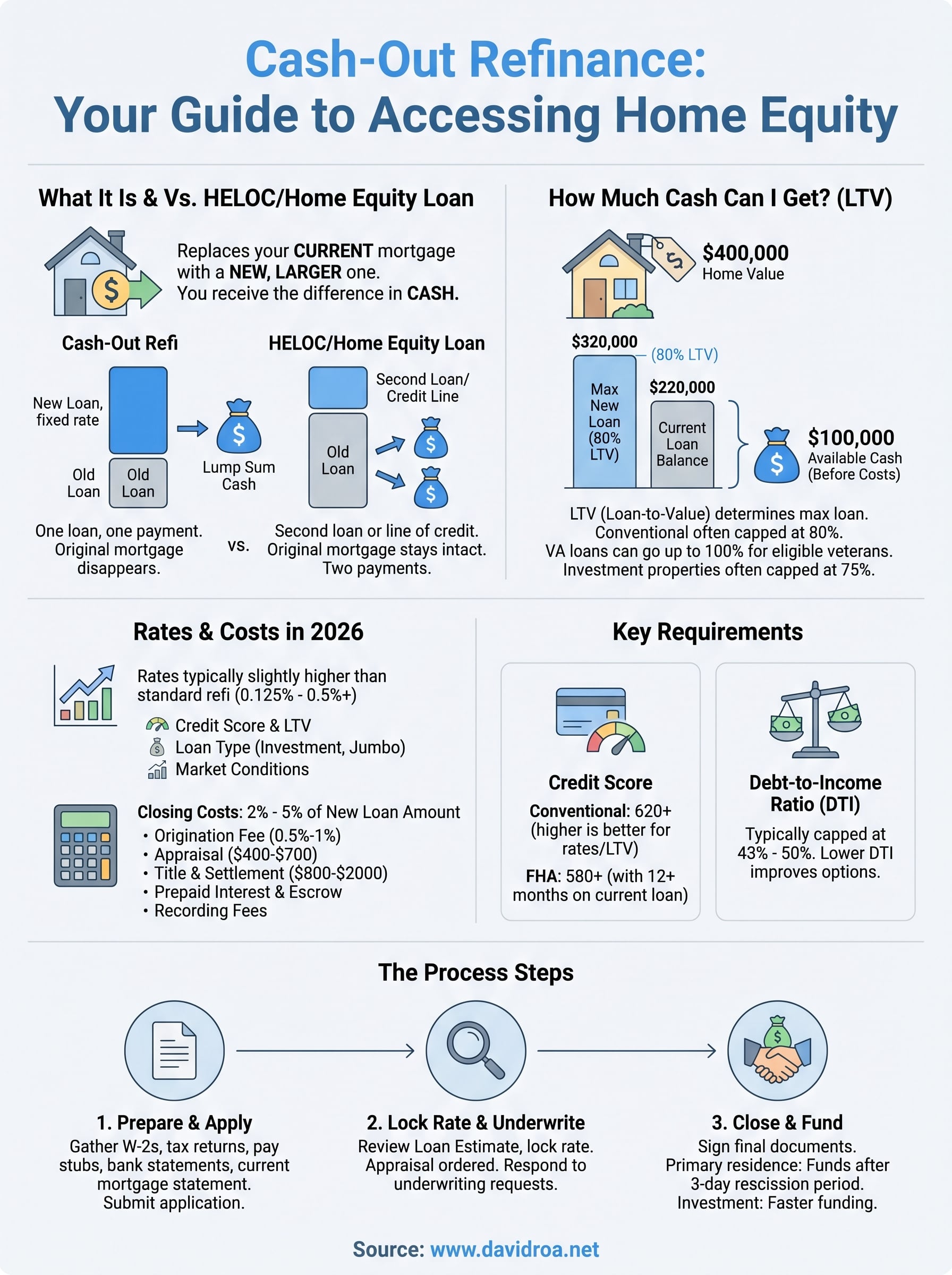

A cash-out refinance replaces your current mortgage with a new, larger loan, and you pocket the difference in cash. Simple concept. But the rates, requirements, and process details vary significantly depending on your credit profile, your property type, and who you work with. Getting it right means understanding the full picture, not just today's rate quote. It also means working with someone who's closed these deals consistently, not just marketed them.

That's where David Roa comes in. With over 25 years in mortgage lending and more than $150 million funded across residential, commercial, and investment deals, I've guided homeowners through every version of this transaction, from straightforward primary residence cash-outs to more complex investor and ITIN scenarios. This article breaks down current rates, eligibility requirements, and each step of the process so you can decide if a cash-out refinance is the right tool for what you're trying to accomplish.

What a cash-out refinance is and how it works

A cash-out refinance works by replacing your existing mortgage with a new, larger loan that covers what you still owe plus the additional amount you want to pull out in cash. The lender pays off your old mortgage, issues a new loan at current terms and rates, and sends you the difference. You walk away with a single monthly payment, a new interest rate, and a lump sum you can use however you need. No second loan. No separate line of credit. One transaction replaces everything.

The difference between a cash-out refi and a home equity loan

Many homeowners confuse a cash-out refinance with a home equity loan or a HELOC. The core difference is structure. With a home equity loan or HELOC, you keep your original mortgage intact and layer a second loan or credit line on top of it. With a cash-out refinance, your original mortgage disappears entirely and gets replaced. That matters because your rate, term, and total loan balance all reset at once. If today's rates are higher than your original rate, a cash-out refi may cost you more over the life of the loan, even if the immediate cash feels useful. If rates are comparable or lower, you could improve your terms while accessing equity at the same time.

| Feature | Cash-Out Refinance | Home Equity Loan | HELOC |

|---|---|---|---|

| Replaces original mortgage | Yes | No | No |

| Rate structure | Typically fixed | Typically fixed | Typically variable |

| Funds delivered as | Lump sum | Lump sum | Revolving credit line |

| Closing costs required | Yes | Yes | Sometimes |

| One monthly payment | Yes | No (you have two) | No (you have two) |

How your loan-to-value ratio controls how much cash you can access

Your loan-to-value ratio (LTV) is the single biggest factor that determines how much you can pull out. Lenders calculate LTV by dividing your new loan amount by your home's appraised value. Most conventional lenders cap cash-out refinances at 80% LTV, which means if your home is worth $400,000, the maximum new loan is $320,000. If you still owe $220,000, you could potentially access up to $100,000 before closing costs. VA loans work differently, and eligible veterans can often refinance up to 100% LTV, making them one of the most powerful cash-out tools available to qualifying borrowers.

The more equity you've built and the lower your remaining balance, the more cash you can access, and staying at or below 80% LTV on a conventional loan also lets you avoid private mortgage insurance on the new loan.

What actually happens at closing and after

When you search cash out refinance near me, what you're really looking for is a lender who can accurately value your property, underwrite your file without unnecessary delays, and close on a reliable timeline. At closing, you sign the new loan documents, and your old mortgage gets paid off at the same time. For primary residences, federal law gives you a three-business-day right of rescission, meaning your cash arrives a few days after signing rather than immediately at the closing table. Investment properties don't carry that waiting period, so funds can be available faster. After closing, your new monthly payment replaces the old one, and your equity position reflects the updated balance against your home's current appraised value. There's nothing additional to track beyond that single new loan.

How to find a cash-out refinance lender near you

When you search cash out refinance near me, the results flood your screen with national banks, online lenders, and local brokers all competing for your attention. The challenge isn't finding options; it's knowing which type of lender actually fits your situation. A large bank may offer competitive rates but slow underwriting. An online lender may be fast but rigid on file complexity. A local mortgage broker often brings the widest product access and the ability to match your specific profile to the right program, which matters most when your scenario isn't straightforward.

What to look for in a lender

Not every lender handles every loan type. Experience with your specific scenario, whether that's a primary residence, an investment property, or an ITIN borrower situation, separates lenders who can actually close your deal from those who will stall midway through underwriting. You want someone who regularly closes cash-out refinances, not someone who occasionally processes them alongside their main volume.

Look for these qualities when evaluating lenders:

- Track record: Ask how many cash-out refinances they've closed in the past 12 months and in what loan categories.

- Product range: A broker with access to multiple wholesale lenders gives you more program options than a single bank with fixed internal guidelines.

- Communication style: Clear timelines and direct answers from the start indicate how the process will go once you're in underwriting.

- Local market knowledge: A lender familiar with your area understands appraisal dynamics, which directly affects how much equity you can actually access.

Questions to ask before you commit

Before you hand over documents, ask each lender the right questions. What is the maximum LTV they allow for your property type, and what will they require if you're pulling cash on an investment property versus a primary residence? These limits vary by lender and by loan program, and knowing them upfront prevents you from starting a process you can't finish.

The difference between an 80% LTV cap and a 75% LTV cap on a $500,000 home is $25,000 in accessible cash, so knowing the ceiling before you apply saves you from surprises at the closing table.

Also ask about the full timeline from application to closing. A lender who tells you 30 days but routinely takes 60 will derail time-sensitive plans, like a property acquisition or a debt payoff with a hard deadline. Ask for their average closing timeline on recent cash-out transactions, not a best-case estimate. That single question will reveal more about how they operate than any marketing page will.

Cash-out refinance rates and costs in 2026

Cash-out refinance rates in 2026 run slightly higher than standard rate-and-term refinance rates, typically by 0.125% to 0.5% depending on your credit score, loan size, and property type. Lenders view cash-out transactions as marginally higher risk because you're increasing your loan balance, so they price that risk into your rate. The gap is not dramatic, but it matters when you calculate the total cost of accessing your equity over the life of the loan.

What drives your rate higher than a standard refinance

Your credit score and LTV combination determines where your rate lands within any lender's pricing grid. Borrowers with scores above 740 pulling cash to 70% LTV will see rates near the top of the market range. Borrowers with scores between 620 and 680 pulling to 80% LTV will see rates meaningfully higher, sometimes by a full percentage point or more. Investment property cash-out refinances carry an additional pricing adjustment on top of that, often 0.5% to 1% higher than an equivalent primary residence transaction, because lenders apply stricter risk overlays to non-owner-occupied properties.

Your loan size also affects pricing. Jumbo cash-out refinances above conforming loan limits follow a separate pricing structure that depends heavily on the lender's appetite for that loan type at a given time.

Closing costs you should plan for

Closing costs on a cash-out refinance typically run 2% to 5% of your new loan amount, and that range covers several distinct line items. Understanding each one helps you compare lender estimates accurately rather than just comparing interest rates.

Here's what makes up the typical cost structure:

- Origination fee: The lender's charge for processing and underwriting your loan, usually 0.5% to 1% of the loan amount

- Appraisal fee: Required for most cash-out transactions; typically $400 to $700 depending on property type and location

- Title insurance and settlement fees: Vary by state but generally range from $800 to $2,000

- Prepaid interest and escrow setup: Covers the days between closing and your first payment, plus initial property tax and insurance deposits

- Recording fees: Local government charges to record the new lien, usually under $200

Some lenders offer no-closing-cost options that roll fees into the loan balance or offset them with a slightly higher rate. That trade-off can make sense if you plan to sell or refinance again within a few years, but it increases the total cost if you hold the loan long term. When you search cash out refinance near me, ask each lender to provide a Loan Estimate within three business days of application so you can compare the full cost picture side by side.

Cash-out refinance requirements and how much you can get

Before you search cash out refinance near me and start comparing lenders, you need to know whether your current financial profile qualifies. Lenders evaluate several factors simultaneously, and each one affects not just your approval odds but also the rate you'll receive and the cash amount you can actually access. Understanding the full picture upfront prevents you from starting a process that stalls in underwriting.

Credit score and debt-to-income thresholds

Your credit score is the first gate lenders check. Most conventional cash-out refinances require a minimum score of 620, though borrowers in the 620 to 679 range will face tighter restrictions on LTV and higher rate adjustments. If your score is 740 or above, you'll qualify for better pricing and more flexible program options. FHA cash-out refinances accept scores as low as 500 in some cases, though most lenders set a practical floor of 580 and require you to have held your current loan for at least 12 months before drawing cash.

Your debt-to-income ratio (DTI) is the second major qualifier. Lenders calculate DTI by dividing your total monthly debt obligations, including the new proposed mortgage payment, by your gross monthly income. Most conventional programs cap DTI at 43% to 50% depending on compensating factors like strong reserves or a high credit score. FHA programs allow slightly more flexibility. If your DTI runs high, reducing other monthly debts before applying will improve your position.

A lower DTI and a higher credit score work together to expand your options, both in terms of which lenders will approve you and how much cash they'll allow you to pull.

How much cash you can actually access

The amount you can pull out depends directly on your home's appraised value, your current loan balance, and the LTV cap your loan program allows. Here's how the math works across common scenarios:

| Home Value | LTV Cap | Max New Loan | Current Balance | Available Cash (Before Costs) |

|---|---|---|---|---|

| $400,000 | 80% | $320,000 | $200,000 | $120,000 |

| $600,000 | 80% | $480,000 | $350,000 | $130,000 |

| $500,000 | 75% (investment) | $375,000 | $250,000 | $125,000 |

VA loans stand apart from this table entirely. If you qualify, the VA cash-out program allows refinancing up to 100% of appraised value, giving eligible veterans significantly more access to their equity than any conventional program. For investment properties, most lenders drop the LTV cap to 75%, which reduces your accessible cash compared to a primary residence transaction at the same property value.

Steps to apply and close without surprises

Once you decide a cash-out refinance fits your goals, the process moves through a predictable sequence. Knowing each stage in advance keeps you from scrambling for documents mid-underwriting or missing a rate lock window because you weren't ready. When you search cash out refinance near me and pick a lender, ask them to walk you through their specific timeline before you sign anything. A lender who can't give you a clear sequence upfront will rarely deliver a smooth close.

Gather your documents before you apply

Lenders need a consistent set of documents to underwrite your file, and getting them together before you submit your application shortens your timeline significantly. Missing paperwork is the most common reason files stall in underwriting, and it's entirely preventable.

Prepare these items before your first lender conversation:

- Last two years of W-2s or tax returns (self-employed borrowers need full returns with all schedules)

- Two most recent pay stubs if you're a W-2 employee

- Two to three months of bank statements covering all accounts you plan to use for reserves

- Current mortgage statement showing your remaining balance and monthly payment

- Homeowners insurance declarations page

- Photo ID and Social Security number for a credit pull

Submit your application and lock your rate

After you submit your application, your lender will issue a Loan Estimate within three business days, which outlines your rate, monthly payment, and total closing costs. Review this document line by line rather than skimming it. Rates move daily, so ask your lender exactly when you can lock your rate and how long that lock stays valid. Most locks run 30 to 60 days, and extending them past that window typically costs money.

Lock your rate as soon as you're confident in the loan terms, because a rate that rises by even 0.25% between application and closing will increase your monthly payment more than most borrowers expect.

Navigate the appraisal and underwriting stage

Your lender will order a home appraisal shortly after your application, and the appraised value directly controls how much cash you can access. Keep the property in good condition before the appraiser visits, since condition affects the final valuation. Underwriting follows the appraisal and involves the lender verifying every document you submitted. Respond to any requests for additional information within 24 to 48 hours to avoid unnecessary delays. Once underwriting issues a clear-to-close, you'll receive final loan documents, sign at closing, and for a primary residence, receive your funds after the three-business-day rescission period ends.

Next steps for your cash-out refi

You now have everything you need to move forward with confidence. You know how the transaction works, what rates and costs to expect, which requirements you need to meet, and how each stage of the process unfolds. The gap between searching cash out refinance near me and actually closing a deal comes down to one thing: working with a lender who knows these deals inside and out and will give you straight answers from day one.

David Roa has funded over $150 million in residential, investment, and commercial loans across more than 25 years in the business. Whether your situation is straightforward or involves an investment property, an ITIN, or a complex income profile, the goal is always the same: get you to closing without surprises. If you're ready to find out exactly how much equity you can access and what it will cost, reach out to David Roa today and get a real answer.