How To Get Preapproved For A VA Loan: Steps & Documents

If you've served in the military, the VA loan benefit is one of the most powerful homebuying tools available to you, but before you start shopping for a home, you need to know how to get preapproved for a VA loan. Preapproval tells sellers you're a serious, qualified buyer, and it gives you a clear picture of what you can actually afford. Without it, you're essentially house hunting blind.

The process itself is straightforward once you understand the steps. You'll need to confirm your eligibility, gather specific financial documents, and work with a lender who handles VA loans regularly. Each piece matters because VA preapproval isn't just a formality, it's a lender's commitment based on a real review of your credit, income, and service history. Getting it right from the start can mean the difference between a smooth closing and a deal that falls apart.

At David Roa, we've helped veterans and active-duty service members secure VA financing as part of the over $150 million in loans we've funded across more than 25 years in the business. VA loans are a core part of our residential mortgage services, and we know exactly what underwriters look for during preapproval. This guide walks you through every step and document you'll need, from obtaining your Certificate of Eligibility to submitting your application, so you can move forward with confidence.

What VA preapproval is and what it is not

Many buyers confuse VA preapproval with other steps in the homebuying process, and that confusion leads to wasted time and avoidable setbacks. Understanding exactly what preapproval means, and what it doesn't cover, gives you a real advantage before you make a single offer.

What VA preapproval actually is

VA preapproval is a conditional commitment from a lender stating you qualify for a VA loan up to a specific dollar amount. To issue it, the lender pulls your credit, verifies your income and employment history, and confirms your VA eligibility through your Certificate of Eligibility (COE). This process involves real underwriting review, not just a quick online calculator estimate. When you finish, you have documented evidence that a lender has evaluated your full financial profile and determined you meet the requirements for VA financing.

A preapproval letter is one of the strongest signals you can send a seller that your offer is backed by verified financing and not just intention.

The letter itself typically includes your approved loan amount, the lender's name, and an expiration date, usually 60 to 90 days from issuance. If your home search runs longer than that window, you'll need to refresh your documents and get an updated letter. Sellers and their agents read these letters carefully, so make sure yours comes from a lender who specializes in VA loans and understands how to get preapproved for a VA loan the right way from day one.

What VA preapproval is not

VA preapproval is not a guarantee of final loan approval. Conditions can arise after you go under contract, including issues with the property appraisal, a change in your employment, or new debt you take on before closing. The lender commits to your financial picture at a specific point in time, which means your responsibility is to keep your finances stable from the date of preapproval all the way through closing day.

Preapproval is also not the same as prequalification. Prequalification is an informal estimate based on numbers you provide yourself, with no document verification and no hard credit pull. It carries almost no weight with experienced sellers in a competitive market. Preapproval, by contrast, requires verified pay stubs, tax returns, bank statements, and a formal credit inquiry. Submitting a prequalification letter when other buyers have full preapproval letters puts you at a direct disadvantage, and in tight markets, sellers will simply move on to the next offer.

Knowing the difference between these two terms, and insisting on true preapproval, is one of the most practical steps you can take before you begin your home search.

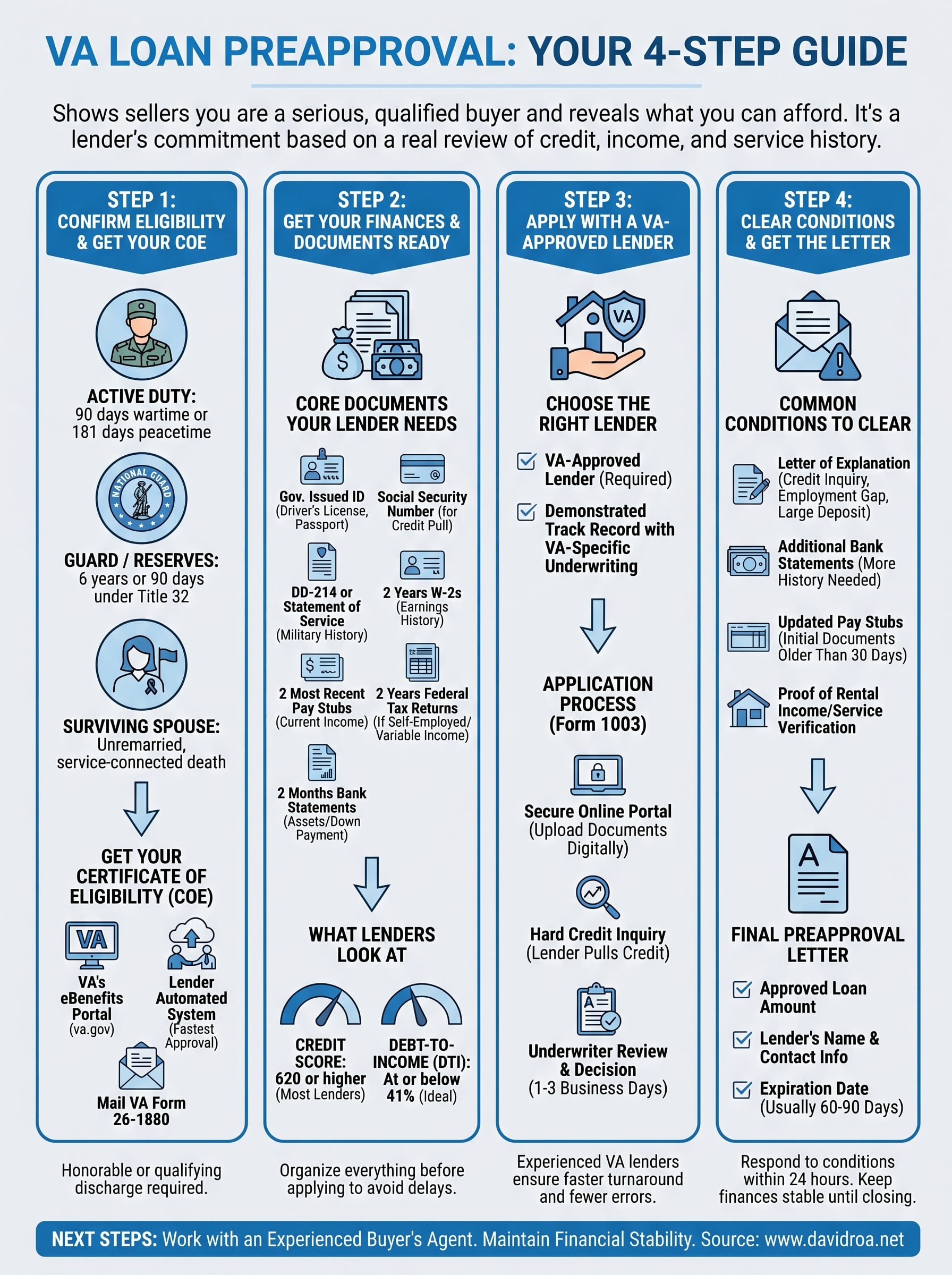

Step 1. Confirm eligibility and get your COE

Before a lender can issue any preapproval, you need to confirm your VA eligibility and obtain your Certificate of Eligibility (COE). The COE is the official document that proves to your lender that you have earned the VA home loan benefit through your military service. Without it, the lender cannot move forward, so this is the first task you need to complete when figuring out how to get preapproved for a VA loan.

Who qualifies for a VA loan

Your eligibility depends on your service history and discharge status. The VA has established minimum active-duty service requirements that vary depending on when and how you served. Here is a quick reference for the most common eligibility categories:

| Service Category | Minimum Service Requirement |

|---|---|

| Active Duty (wartime) | 90 continuous days |

| Active Duty (peacetime) | 181 continuous days |

| National Guard / Reserves | 6 years, or 90 days under Title 32 |

| Surviving Spouse | Unremarried spouse of a veteran who died in service or from a service-connected disability |

Discharge status also matters: you need an honorable or qualifying discharge to be eligible. If your discharge was anything other than honorable, contact the VA directly at va.gov to review your specific situation before applying.

How to request your COE

You have three options to get your COE: through the VA's eBenefits portal at va.gov, through your lender directly using the VA's automated system (most VA-approved lenders can pull it on your behalf in minutes), or by mailing VA Form 26-1880 to your regional VA loan center.

The fastest route is to let your lender request the COE through the VA's automated system, since most approvals come back the same day.

Working with an experienced VA lender means this step often happens in the background while you move on to gathering your financial documents.

Step 2. Get your finances and documents ready

Once you have your COE in hand, you need to shift focus to your financial documents. Lenders underwrite VA loans based on your actual income, credit history, and assets, so organizing everything before you apply will save you from delays and back-and-forth requests after you submit. The more prepared you are at this stage, the faster the lender can complete the review.

The core documents your lender will need

Your lender needs to verify your identity, income, and financial stability through specific documentation. Missing even one item can stall your file, so gather everything before you submit your application.

| Document | Details |

|---|---|

| Government-issued ID | Driver's license or passport |

| Social Security number | Required for credit pull |

| DD-214 or Statement of Service | Confirms military service history |

| Two years of W-2s | Shows employment and earnings history |

| Two most recent pay stubs | Confirms current income |

| Two years of federal tax returns | Required if self-employed or have variable income |

| Two months of bank statements | Verifies assets and down payment funds |

| Certificate of Eligibility | Already obtained in Step 1 |

If you have additional income sources like rental income or freelance work, bring documentation for those too, since lenders can use verified secondary income to strengthen your overall borrower profile.

What lenders look at in your credit and income

Your credit score and debt-to-income ratio (DTI) are the two numbers that carry the most weight during VA preapproval. The VA itself does not set a minimum credit score, but most VA-approved lenders require a score of at least 620. Your DTI should ideally sit at or below 41 percent, though lenders can approve higher ratios if your other factors are strong. Pay off any small revolving balances you can before applying, and avoid opening new credit accounts while you are learning how to get preapproved for a VA loan.

Step 3. Apply with a VA-approved lender

With your documents organized and your COE ready, you can submit a formal application. Not every mortgage lender handles VA loans with the same level of experience, and who you choose at this stage directly affects how smoothly your preapproval moves through underwriting. Applying with a lender who processes VA loans regularly means fewer errors, faster turnaround, and a loan officer who already knows what underwriters need before conditions come back.

Choose the right lender

Your lender must be VA-approved, meaning they are authorized by the Department of Veterans Affairs to originate and process VA loans. Beyond that basic requirement, look for a lender with a demonstrated track record with VA-specific underwriting, not just a general mortgage operation that happens to offer VA products on the side. Ask directly how many VA loans they close per year and what their average time to preapproval is. A lender who hedges on those answers is a lender you should move past.

Choosing a lender who treats VA loans as a specialty, rather than an occasional product, is one of the most practical decisions you can make when figuring out how to get preapproved for a VA loan.

What the application process looks like

Once you select your lender, you will complete a Uniform Residential Loan Application, commonly called the 1003 form. This form captures your personal information, employment history, income, assets, and the property details if you have a specific home in mind. Most lenders now offer a secure online portal where you can upload your documents and complete the 1003 digitally, which speeds up the review. After you submit, the lender pulls a hard credit inquiry and assigns your file to an underwriter for review. From that point, a decision on your preapproval letter typically comes back within one to three business days, depending on the lender's volume and how complete your file is.

Step 4. Clear conditions and get the letter

After your lender submits your file to underwriting, you will likely receive a conditional approval before the final preapproval letter. This is normal and does not mean something went wrong. Conditions are specific items the underwriter needs to verify before issuing the letter. How quickly you respond to conditions directly determines how fast you get your preapproval letter in hand.

What conditions commonly look like

Conditions vary by borrower, but most fall into predictable categories. Understanding what to expect when figuring out how to get preapproved for a VA loan helps you respond immediately rather than letting your file sit idle.

Common conditions include:

- Letter of explanation for a credit inquiry, gap in employment, or large deposit

- Additional bank statements if the underwriter needs more months of history

- Updated pay stubs if your initial documents are older than 30 days

- Proof of rental income if you listed it on your application

- Verification of military service if your COE needs supplemental documentation

Respond to every condition within 24 hours. Underwriters work multiple files at once, and slow responses push your file to the back of the queue.

How to get the final letter

Once you clear all conditions, the underwriter issues a clear to proceed, and your loan officer generates the preapproval letter. Read the letter carefully before you use it. Confirm the approved loan amount matches what you discussed, check the expiration date, and verify the lender's contact information is current. If anything looks off, call your loan officer immediately and request a corrected version.

Your preapproval letter is a working document, so store a digital copy accessible from your phone. You will need to submit it alongside every offer you make.

Next steps after preapproval

Your preapproval letter is active, and now the real work begins. Start your home search with a buyer's agent who has experience working with VA financing, since VA loans have specific appraisal requirements that not every agent handles well. Stay disciplined about your finances during this period: avoid large purchases, new credit accounts, or job changes, because any of those can unwind your approval before you reach closing. Once you find a property and go under contract, your lender will order the VA appraisal and move your file into full underwriting for final loan approval.

Knowing how to get preapproved for a VA loan is the foundation, but executing the process correctly requires a lender who handles VA files every day. At David Roa, we bring over 25 years of mortgage experience and a direct understanding of what VA underwriters need. Start your VA loan preapproval with David Roa and get the financing your service earned.