What Is The Jumbo Loan Limit In 2026? FHFA Thresholds

If you're shopping for a home priced above the average range, one of the first questions you'll run into is what is the jumbo loan limit, and the answer directly affects your loan options, interest rate, and down payment requirements. For 2026, the Federal Housing Finance Agency (FHFA) has set new conforming loan limits that determine exactly where conventional financing ends and jumbo territory begins.

The threshold isn't the same everywhere. Standard areas carry one baseline limit, while high-cost markets, think parts of California, New York, and Hawaii, get a higher ceiling. Knowing which number applies to your purchase can save you from unnecessary costs or steer you toward a loan product that actually fits your situation. With over 25 years in mortgage lending and more than $150 million funded, I've walked hundreds of borrowers through this exact decision at David Roa.

This article breaks down the 2026 FHFA conforming loan limits, explains how they're calculated, covers the differences between standard and high-cost areas, and outlines what jumbo loan requirements look like once you cross that line. Whether you're buying a primary residence or adding to an investment portfolio, you'll leave with the numbers and context you need to move forward.

Why the jumbo loan limit matters

When you ask what is the jumbo loan limit, you're really asking where your financing options split into two very different paths. A loan that stays at or below the conforming limit qualifies for purchase by Fannie Mae or Freddie Mac, which means lenders can sell it on the secondary market and offer you more competitive terms. The moment your loan amount crosses that line, you move into jumbo territory, and the rules governing your approval, rate, and required reserves shift considerably.

Your loan options change at the threshold

Conforming loans come with standardized guidelines that most lenders follow closely. Because Fannie Mae and Freddie Mac back these loans, the risk stays low for the lender, and that lower risk translates directly into more accessible approval standards for you. You can qualify with a lower credit score, put less money down in some cases, and benefit from a large pool of lenders competing for your business, which creates real leverage when you're shopping rates.

Once you exceed the conforming limit, you're borrowing money the lender keeps on its own books or sells through private channels. That means each lender sets its own jumbo guidelines, which vary considerably from one institution to the next. Some require a 20 percent down payment as a minimum, others want to see 12 months of cash reserves, and credit score requirements often jump to 700 or higher. The practical effect is that two borrowers with identical financial profiles can receive very different terms depending on which lender they approach.

Crossing the jumbo threshold doesn't just change your loan type; it changes how every part of your application gets evaluated.

Rates, reserves, and down payments shift too

Interest rates on jumbo loans have historically run higher than conforming rates, though the gap has narrowed in recent years. The key point is that rate differences of even 0.25 to 0.50 percent on a $1.2 million loan can add tens of thousands of dollars in total interest over a 30-year term, so understanding exactly where the limit falls has a direct impact on your long-term housing costs.

Your required cash reserves also increase in jumbo scenarios. Lenders typically want to see six to twelve months of mortgage payments sitting in verifiable accounts after closing, a standard that most conforming borrowers never face. If your purchase price sits just above the limit, it's worth running the numbers on a piggyback loan structure, where a second loan covers the gap and keeps your first mortgage under the conforming ceiling. That one move can eliminate the jumbo classification entirely and put you back into a more competitive lending environment.

What sets the jumbo loan limit in 2026

The answer to what is the jumbo loan limit starts with a single federal agency: the Federal Housing Finance Agency (FHFA). Each fall, the FHFA reviews home price data from across the country and adjusts the conforming loan limits for the following year. Those limits define the maximum loan amount Fannie Mae and Freddie Mac will purchase, and anything above those figures becomes a jumbo loan by definition.

How the FHFA calculates the annual adjustment

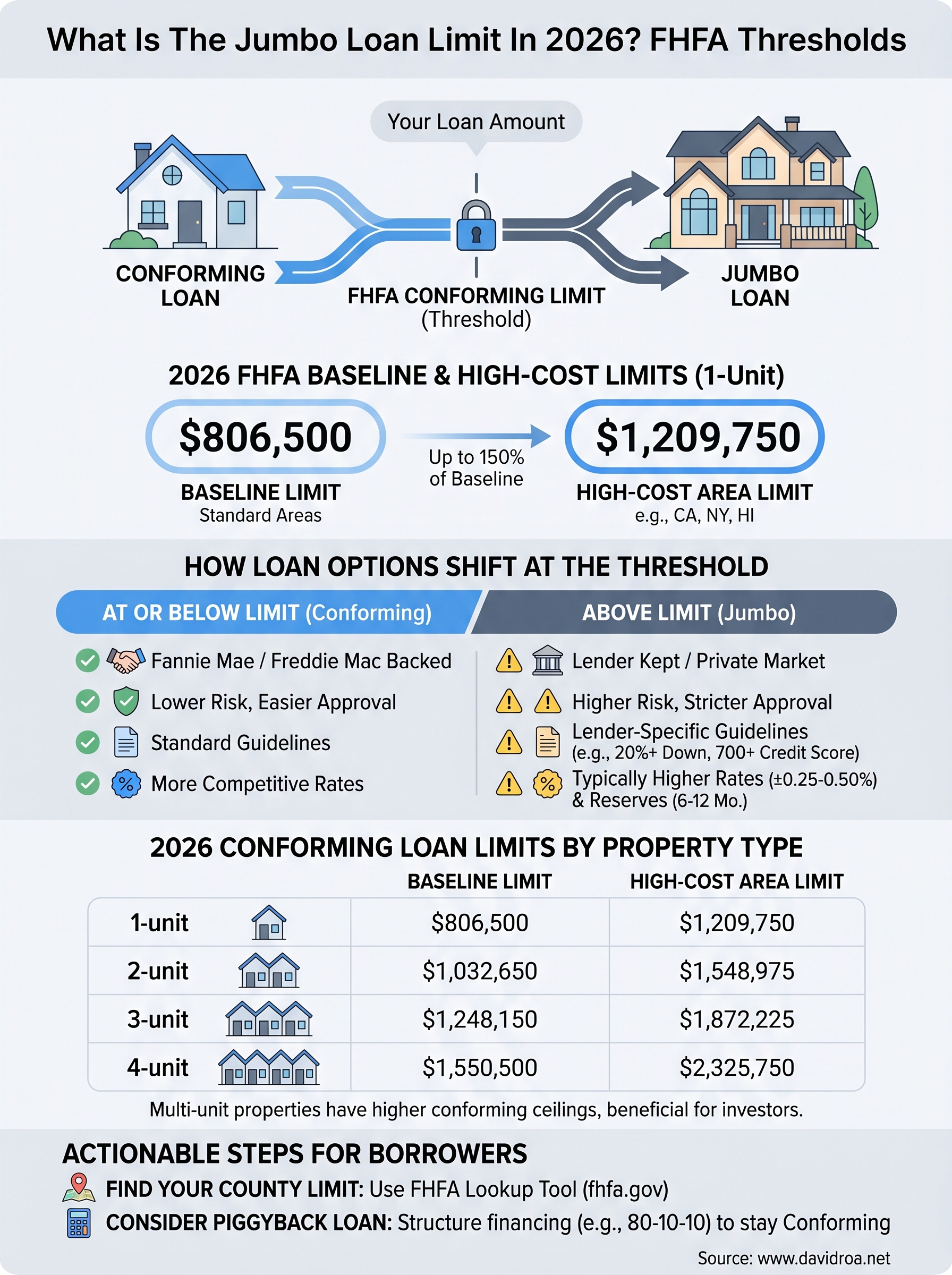

The FHFA uses the House Price Index (HPI), a measure of home value changes across the country, to set each year's limit. When home prices rise nationally, the conforming limit increases by a corresponding percentage. For 2026, that calculation produced a baseline conforming limit of $806,500 for a single-unit property in most U.S. counties. This number applies to the majority of markets where home prices track near the national average.

The baseline limit moves in step with national home price growth, so it reflects real market conditions rather than an arbitrary figure.

The high-cost area exception

Congress recognized that some markets have home prices far above the national median, so the law allows the FHFA to set higher conforming limits in those areas. High-cost counties can receive a limit up to 150 percent of the baseline, which works out to $1,209,750 for a single-unit property in 2026. Markets like San Francisco, Honolulu, and the New York City metro area typically qualify for this elevated ceiling, which keeps more buyers in conforming loan territory without requiring a jumbo product.

Your specific county determines which number applies to your purchase, so checking the FHFA lookup tool for your location is a necessary first step before you decide on a loan structure.

2026 conforming loan limits by property type

The number you need to watch when asking what is the jumbo loan limit depends on more than just your county. The FHFA sets separate limits for properties with one to four units, which means a duplex, triplex, or four-plex purchase triggers a higher conforming ceiling before you cross into jumbo territory. Understanding these unit-based thresholds is especially useful if you're building a rental portfolio and want to keep your financing costs as low as possible.

A multi-unit purchase gives you a higher conforming ceiling, which can keep your loan conventional even on a significant investment property.

Baseline and high-cost limits for each unit count

The table below shows the 2026 conforming loan limits for both standard and high-cost counties across all four property types:

| Property Type | Baseline Limit | High-Cost Area Limit |

|---|---|---|

| 1-unit | $806,500 | $1,209,750 |

| 2-unit | $1,032,650 | $1,548,975 |

| 3-unit | $1,248,150 | $1,872,225 |

| 4-unit | $1,550,500 | $2,325,750 |

These figures apply to loans originated in 2026 and reflect the FHFA's annual adjustment based on national home price data. If your loan amount falls at or below the figure matching your property type and county, you qualify for conventional financing rather than a jumbo product.

Why the unit count matters for investors

Real estate investors often overlook the multi-unit scaling built into conforming limits. A two-unit property in a standard county carries a $1,032,650 ceiling, meaning you can finance a duplex at that price point with a conforming loan and avoid stricter jumbo reserve requirements. The four-unit baseline of $1,550,500 is particularly relevant for investors pursuing house-hacking strategies or small apartment acquisitions, since staying under that ceiling keeps lender guidelines and approval criteria far more manageable.

How to find your county jumbo threshold

Knowing the national baseline answers part of the question of what is the jumbo loan limit, but your purchase decision ultimately depends on the limit assigned to the specific county where the property sits. The FHFA publishes county-level conforming loan limits every year, and looking up your county takes less than two minutes using the right source.

Use the FHFA lookup tool

The FHFA maintains a searchable database at fhfa.gov that lists the conforming loan limit for every county and county-equivalent in the United States. You can search by state, county name, or metropolitan statistical area to pull the exact figure that applies to your target property. The result tells you the 2026 limit for each unit count, from a single-family home all the way up to a four-unit building.

Pull the limit for your specific county before you finalize any purchase price strategy, because high-cost designations can shift by a few miles across county lines.

When you find your county's limit, compare it directly to your anticipated loan amount, not your purchase price. Your loan amount reflects your purchase price minus your down payment, so even a home priced above the limit can stay in conforming territory if your down payment is large enough to bring the financed portion below the ceiling.

When your county sits on the boundary

Some counties receive limits between the $806,500 baseline and the $1,209,750 high-cost ceiling, which means they fall into a mid-range category. These counties saw significant home price growth but didn't qualify for the full 150 percent adjustment. If your county lands in this middle range, the exact dollar figure from the FHFA table is the only number that matters for your loan classification, so avoid estimating based on neighboring counties.

How to plan a purchase above the limit

Once you know what is the jumbo loan limit for your county and confirm your loan amount will exceed it, your planning process needs to start earlier than it would for a standard conforming purchase. Jumbo lenders scrutinize your full financial picture more carefully than conforming guidelines require, so giving yourself at least 90 days before a target closing date allows you to address any gaps before they become problems.

Consider a piggyback loan structure

One of the most effective ways to avoid jumbo requirements is to split your financing into two loans. A piggyback structure, often called an 80-10-10, pairs a conforming first mortgage with a second loan or home equity line that covers the gap between your down payment and the conforming ceiling. This keeps your primary loan within Fannie Mae or Freddie Mac guidelines and eliminates the stricter reserve and credit requirements that come with jumbo products.

The tradeoff is that you carry two separate loans with two sets of terms. Compare the combined monthly payment and total interest cost against a straight jumbo loan before committing to either path. In some scenarios, a well-priced jumbo loan from a portfolio lender beats the piggyback structure on overall cost.

Running both scenarios with actual rate quotes gives you a concrete comparison rather than a guess.

Prepare your financial profile early

Jumbo lenders typically want a credit score of 700 or higher, six to twelve months of verified cash reserves after closing, and a debt-to-income ratio under 43 percent. If any of those areas need work, address them before you start submitting applications. Paying down revolving balances, consolidating accounts, and documenting all asset sources clearly can meaningfully strengthen your file and expand the lender options available to you.

Next steps

You now have a clear answer to what is the jumbo loan limit in 2026, along with the county-level context and financial preparation steps you need to act on that information. The 2026 baseline sits at $806,500 for a single-unit property in standard counties, and high-cost areas extend that ceiling to $1,209,750. Multi-unit properties carry higher thresholds that can keep investor financing in conforming territory even at significant purchase prices.

Your next move is to pull your county's specific limit from the FHFA lookup tool, calculate your actual loan amount based on your target down payment, and then compare a conventional structure against a jumbo or piggyback alternative using real rate quotes. Getting those numbers in front of an experienced lender early removes uncertainty and gives you time to strengthen your file before you need to close. If you're ready to run those numbers on a purchase or refinance, connect with David Roa to get started.