Cash-Out Refinance for Home Improvements: How It Works

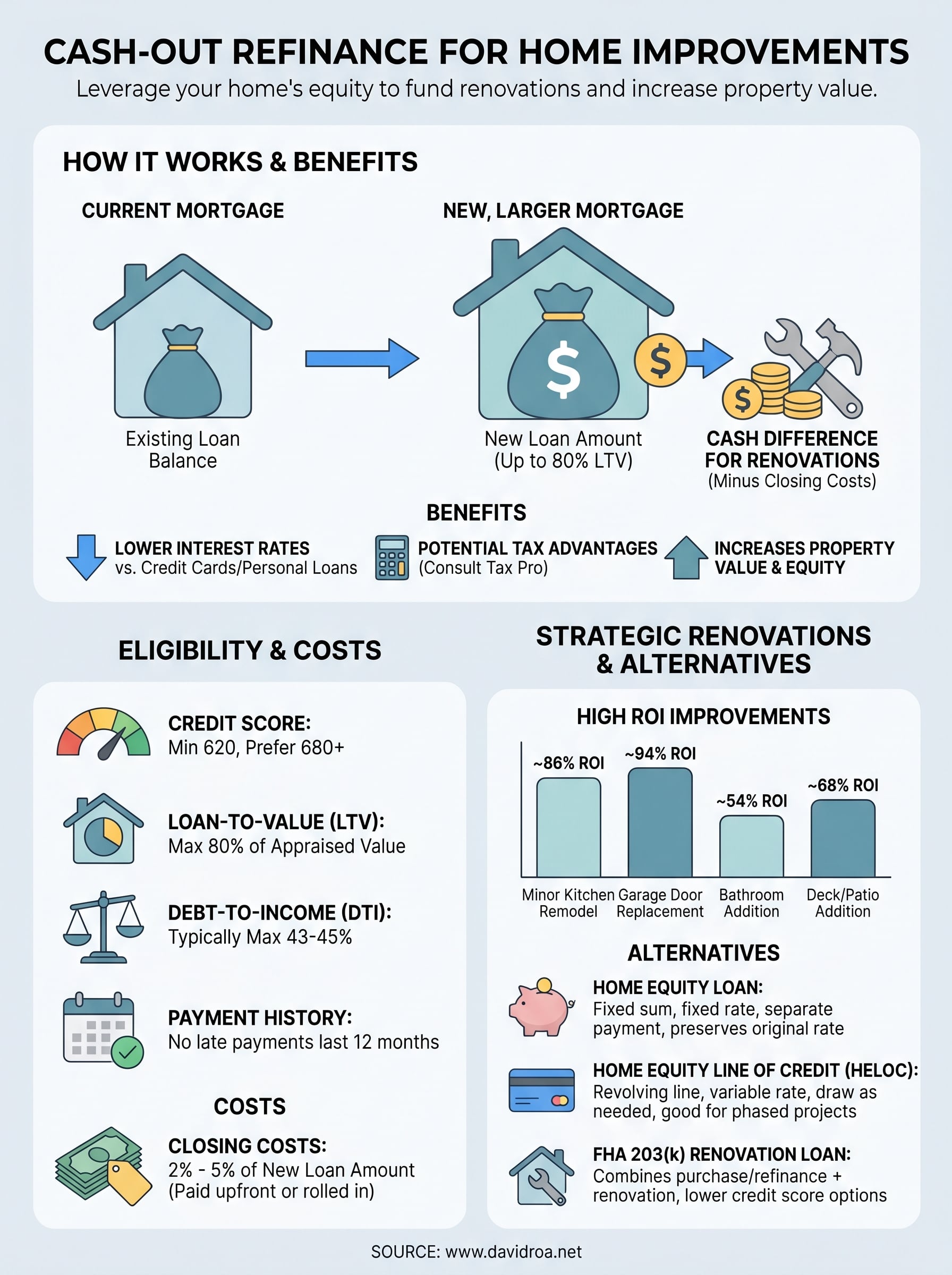

Your home is sitting on equity you've already earned, and if you're planning a kitchen remodel, a new roof, or a full renovation, a cash-out refinance for home improvements lets you put that equity to work. Instead of racking up high-interest credit card debt or draining your savings, you replace your current mortgage with a larger one and receive the difference in cash to fund the upgrades your property needs.

It's one of the most practical ways homeowners finance renovations, but the process involves more moving parts than a standard refinance. You need to understand how lenders evaluate your equity position, what the eligibility requirements look like, and whether the numbers actually make sense for your situation. Getting this wrong can cost you thousands over the life of your loan, getting it right can increase your property's value well beyond what you borrow.

At David Roa, we've funded over $150 million in residential and investment loans across more than 25 years in the business. We work with homeowners every day who want to leverage their equity for improvements, and we know exactly where the opportunities and pitfalls are. This guide breaks down how a cash-out refinance works step by step, what you'll need to qualify, and how to use the funds strategically so your renovation adds real value to your home.

Why homeowners use it for improvements

A cash-out refinance gives you access to a large lump sum at mortgage interest rates, which are typically lower than personal loans, home equity lines of credit, or credit cards. When you're looking at a $40,000 kitchen renovation or a $60,000 addition, the difference in rate between a mortgage and a credit card can translate to tens of thousands of dollars over the repayment period. That spread is exactly why so many homeowners choose this route over other financing options when tackling large-scale projects.

The cost of renovations keeps climbing

Construction costs, materials, and labor have risen significantly over the past several years. Average kitchen remodels now run between $25,000 and $80,000 depending on scope and location, and bathroom renovations often start at $15,000 for anything beyond basic cosmetic updates. Most homeowners don't have that kind of cash sitting in a savings account, and building up those funds while costs keep rising means your renovation budget shrinks every year you wait.

Using your home's equity to fund improvements is often more cost-effective than waiting to save the full amount outright, because the renovation cost you avoid tomorrow is worth more than the interest you pay today.

Your equity works harder than a personal loan

When you use a cash out refinance for home improvements, you're borrowing against an asset you already own. Personal loans are unsecured, which means lenders charge higher rates to offset their risk, while your home acts as collateral in a refinance so lenders extend better terms. Interest on mortgage debt used for home improvements is also potentially tax-deductible, which is a benefit personal loan borrowers don't get. Consult a tax professional to confirm how this applies to your specific situation.

Monthly payments on a cash-out refinance spread over 15 to 30 years keep the monthly obligation manageable compared to a personal loan with a 3-to-5-year repayment window. For a major renovation, cash flow control matters as much as the total interest cost, and a refinance gives you the flexibility to fund large projects without straining your budget every month.

Improvements that increase your home's market value

Not every renovation returns equal value when you sell. The projects that consistently produce the strongest return on investment are ones that address buyer priorities and improve core functionality.

| Improvement | Avg. Cost | Est. ROI |

|---|---|---|

| Minor kitchen remodel | $26,000 | 86% |

| Garage door replacement | $4,000 | 94% |

| Bathroom addition | $50,000 | 54% |

| Deck or patio addition | $17,000 | 68% |

Strategic renovations funded through a cash-out refinance can raise your home's appraised value, which strengthens your equity position for any future financing needs. You borrow against the equity you have now and, if you pick the right improvements, you build even more equity in the process.

How the process works from start to finish

A cash out refinance for home improvements follows the same basic path as your original mortgage, but with one key difference: your lender pays off your existing loan and issues a new, larger one, sending you the difference in cash at closing. The entire process typically takes 30 to 45 days from application to funding, though your timeline can shift based on lender workload and how quickly you gather documentation.

Getting your application in order

Before your lender can move forward, you need to submit a full mortgage application along with supporting financial documents. This includes recent pay stubs, W-2s or tax returns for the past two years, bank statements, and your current mortgage statement. Having these ready before you apply shortens the processing time considerably and reduces unnecessary back-and-forth with underwriting.

Here's what most lenders request upfront:

- Pay stubs from the last 30 days

- W-2s or tax returns for the past two years

- Bank statements from the last two to three months

- Current mortgage statement

- Photo ID and proof of homeowners insurance

Appraisal, underwriting, and closing

Once you submit your application, your lender orders a home appraisal to confirm your property's current market value. The appraised value sets the ceiling on how much equity you can access, so the condition of your home and comparable sales in your area directly affect your loan amount. After the appraisal, underwriters review your full file to verify income, credit, and your loan-to-value ratio.

The appraisal is often the step that surprises borrowers most, because it can either expand or limit your borrowing power depending on current market conditions in your area.

When underwriting clears your file, you move to closing, where you sign your new loan documents. Federal law then requires a three-day rescission period before your funds are released, so plan your renovation start date accordingly.

How much you can borrow and the true cost

Most lenders cap your new loan at 80% of your home's appraised value, which means your equity position directly determines how much cash you can pull out. If your home is worth $400,000 and you owe $250,000, your available equity is $150,000, but you can only access up to $70,000 after accounting for the 80% cap ($320,000 maximum loan minus the $250,000 balance).

Calculating your maximum cash-out amount

Your loan-to-value ratio (LTV) is the number lenders use to set your borrowing ceiling. To find your maximum cash-out amount, multiply your home's appraised value by 0.80, then subtract your current mortgage balance. The result is what you can receive before closing costs.

| Home Value | 80% Cap | Current Balance | Max Cash Out |

|---|---|---|---|

| $300,000 | $240,000 | $180,000 | $60,000 |

| $400,000 | $320,000 | $250,000 | $70,000 |

| $500,000 | $400,000 | $280,000 | $120,000 |

The real cost you need to factor in

A cash out refinance for home improvements carries closing costs between 2% and 5% of the new loan amount, and those costs either come out of pocket or roll into your loan balance. Rolling them in reduces your cash received and slightly increases your monthly payment, so factor this into your renovation budget before you commit to a project scope.

The most common mistake borrowers make is calculating their maximum borrowing amount without subtracting closing costs, which leaves them short on renovation funds at the worst possible time.

Your interest rate on the new loan also drives total cost over the full term. Refinancing from a lower rate to a higher one can add tens of thousands in interest across 30 years, so run the complete numbers rather than focusing only on how much cash you receive at closing.

Eligibility rules lenders use

Before you can tap your equity through a cash out refinance for home improvements, lenders run your file through a set of standard eligibility criteria. These requirements exist to protect both you and the lender from overleveraging a property, and understanding them upfront saves you from surprises during underwriting. Meeting these benchmarks doesn't guarantee approval, but falling short on even one of them can stall or block your application entirely.

Credit score and equity minimums

Most conventional lenders require a minimum credit score of 620, though you'll access better rates at 680 or above. Your credit score directly affects your interest rate, so borrowers who sit just above the minimum threshold often pay significantly more over the life of the loan than those with stronger profiles. On the equity side, lenders generally require you to retain at least 20% equity in your home after the cash-out is complete, which is why the 80% LTV cap discussed earlier is the industry standard rather than an exception.

Checking your credit report before you apply gives you time to dispute errors or pay down revolving balances, both of which can lift your score in 30 to 60 days.

Debt-to-income ratio and payment history

Your debt-to-income ratio (DTI) measures your total monthly debt obligations against your gross monthly income. Most lenders cap DTI at 43% to 45% for a cash-out refinance, meaning your new mortgage payment plus all other recurring debts must fall within that range. Beyond DTI, lenders also review your mortgage payment history, and most require no late payments in the previous 12 months. A single missed payment within that window can push you into a higher-risk category or disqualify you with certain loan programs altogether.

Alternatives to a cash-out refinance

A cash out refinance for home improvements makes sense in many situations, but it's not the only path to renovation funding. If your current mortgage carries a low interest rate you don't want to give up, or if your project scope is smaller, one of these alternatives may fit your situation better without resetting your entire loan.

Home Equity Loan

A home equity loan lets you borrow against your equity in a lump sum while keeping your existing mortgage completely separate. You make two monthly payments instead of one, but your original loan rate stays untouched. This option works well when you have a specific renovation budget and want predictable fixed monthly payments without touching your primary mortgage terms.

A home equity loan is worth comparing directly against a cash-out refinance whenever your current mortgage rate is lower than today's refinance rates.

Home Equity Line of Credit

A HELOC gives you a revolving credit line tied to your home's equity, similar to a credit card but secured by your property. You draw funds as needed during the draw period rather than receiving everything upfront, which works well for phased renovation projects where costs arrive in stages. Rates are typically variable, so your payment can shift over time based on market conditions.

FHA 203(k) Renovation Loan

The FHA 203(k) loan wraps your purchase or refinance amount and renovation costs into a single mortgage. If you're buying a fixer-upper or your home needs structural repairs, this program lets you finance both under one loan with lower credit score thresholds than most conventional options require. It's especially useful for borrowers who don't yet have enough equity built up for a cash-out refinance.

Key takeaways and next steps

A cash out refinance for home improvements gives you access to your equity at mortgage rates, but the math only works when you run the full numbers before you commit. Your borrowing limit sits at 80% of your home's appraised value, and closing costs between 2% and 5% reduce the actual cash you receive at closing. The strongest candidates carry credit scores above 680, maintain at least 20% equity after the transaction, and keep their debt-to-income ratio below 45%.

Pick renovations that build real market value rather than just personal preference, and compare the refinance option against a home equity loan or HELOC if your current rate is worth keeping. Your timeline, equity position, and credit profile all shape which product fits best. If you want to work through the numbers with a lender who has closed over $150 million in loans, reach out to David Roa to find the right financing path for your property.